CEO Report: The Income Tax Will Become Law

What Happens Next Will Decide What Kind of State We Become

Later today, the Washington House of Representatives is expected to pass legislation creating a 9.9% income tax with a $1 million exemption. The Senate is expected to quickly concur, and the Governor has already said he will sign it.

That decision will likely trigger years of legal challenges, a ballot initiative campaign, and significant uncertainty around Washington’s tax structure.

Supporters argue the tax is necessary to stabilize the budget, address regressivity, fund education, and offset federal cuts. But when the numbers are examined closely, these arguments become much harder to sustain.

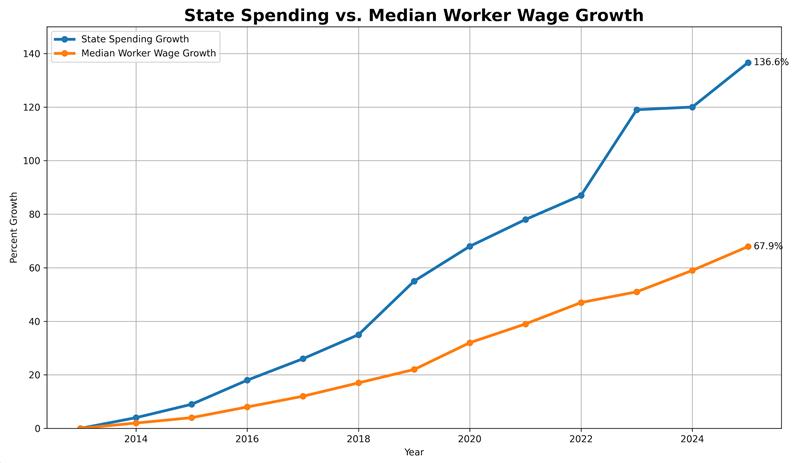

It’s a Spending Problem, Not a Revenue Problem

The Senate’s long‑term outlook assumes the new tax will generate about $2.3 billion annually by fiscal year 2029, but even that revenue does not stabilize the budget. According to the Senate’s own projections, $1.3 billion of the income-tax revenue will be needed just to preserve what the state calls “maintenance-level” spending. That leaves roughly $1 billion in reserves.

There’s one problem, though: The projection assumes spending will grow only 2.2 percent in the next biennium. Over the past decade, Washington spending has grown about 15 percent per biennium on average, with the lowest increase still coming in at 11.3 percent. The 2.2 percent projection doesn’t include many of the most significant cost drivers in Olympia, like the state employee collective bargaining agreements, which alone are estimated to be in the $3 to $5 billion range.

“If spending grows even at the lowest historical rate, every dollar of the new income-tax revenue will be consumed.”

If spending grows even at that lowest historical rate, every dollar of projected income‑tax revenue will be consumed, and the state will still face a deficit of roughly $7-10 billion in the following biennium. Just last year the legislature passed what was widely described as the largest tax increase in Washington state history.

“When tax increases become annual events, they stop being solutions and start becoming symptoms.”

You can like the income tax, hate the income tax, or be somewhere in between, but the math makes one thing difficult to deny: It is highly unlikely the tax will remain limited to millionaires if the state can’t get its spending under control.

“It’s highly unlikely the tax will remain limited to millionaires if the state can’t get its spending under control.”

The state’s fiscal challenges are also connected to decisions made during, and after the pandemic. Unlike most private businesses, the Washington state government did not conduct significant COVID‑era layoffs, and instead, large amounts of one‑time federal pandemic relief funding were used to create new ongoing programs.

Between 2021 and 2025 the state added nearly 10,000 employees, not including schools or universities. While that number has since declined somewhat, Washington still employs roughly 8,000 more state workers than it did before the pandemic, and the long‑term cost of those positions runs into the billions annually.

Many states responded to the pandemic by streamlining government operations to remain competitive with the private sector. Just last week, Utah cut $275 million for its budget and returned $123 million to taxpayers.

Washington has moved aggressively in the opposite direction.

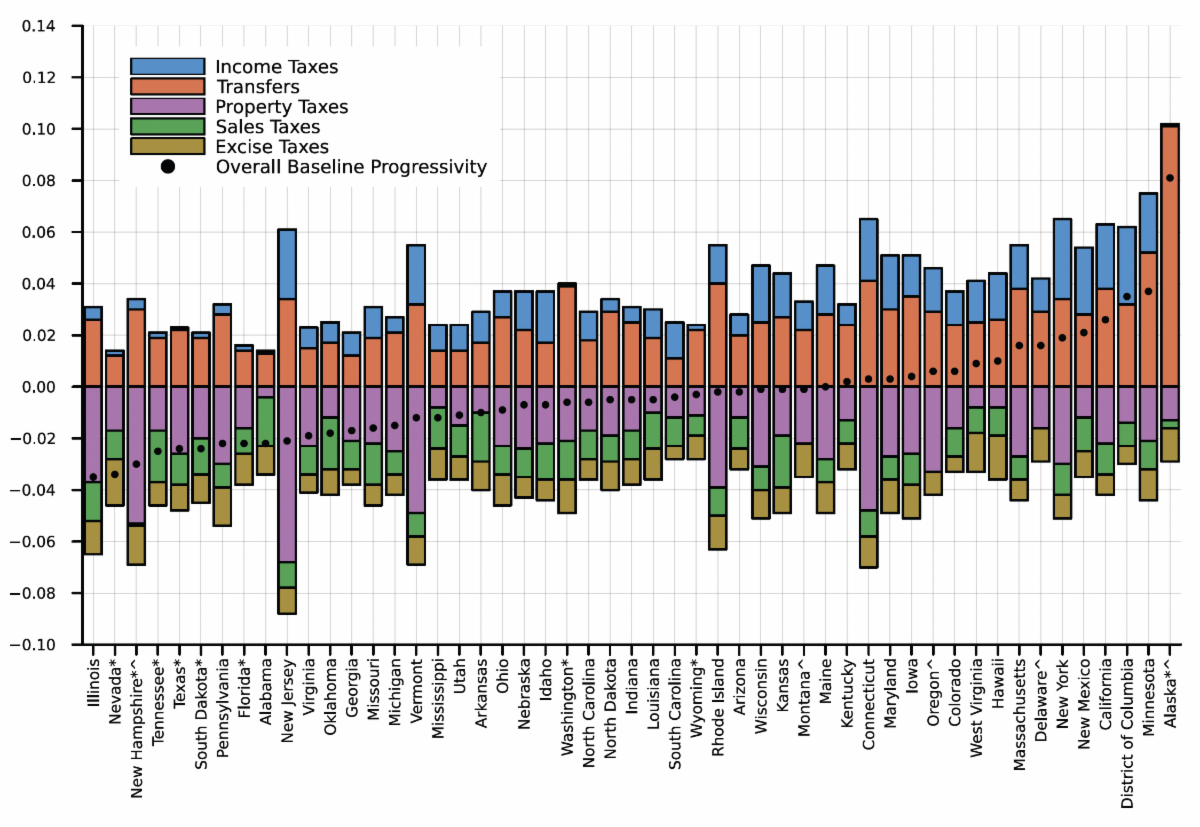

The Regressivity Debate

Supporters of the income tax often argue that Washington’s tax system must be rebalanced because it is one of the most regressive in the nation.

That claim largely stems from research produced by the Institute on Taxation and Economic Policy (ITEP). Their analysis assumes business taxes are largely passed along to consumers through higher prices. Because of that assumption, Washington’s Business and Occupation tax is treated similarly to a sales tax when calculating regressivity.

Since Washington relies heavily on consumption-based taxes, that methodology pushes the state toward the top of those rankings. Especially after last year when legislators massively increased the B&O tax, making the state even more regressive based on ITEP’s methodology.

However, other academic research tells a more nuanced story. Studies by economists affiliated with the Federal Reserve Bank of Minneapolis and Princeton University find that when taxes and government transfers are considered together, Washington appears much closer to the middle of the national pack.

Even if one accepts the premise that Washington’s tax system should be made more progressive, the structure of the proposal raises another important question.

Only about 27 percent of the projected revenue from the income-tax proposal before lawmakers today is aimed at reducing other, “regressive” taxes. Some of the taxes that are reduced will also cut funding to county governments. In exchange, those counties will have the authority to increase regressive sales taxes to fill the hole. A policy framed as “progressive tax reform” that devotes only a quarter of its revenue to reforming the tax code is, in practice, just a tax increase.

That means roughly three-quarters of the revenue goes toward new or expanded spending rather than lowering existing burdens such as some of the highest sales, gas, property, and B&O taxes in the nation.

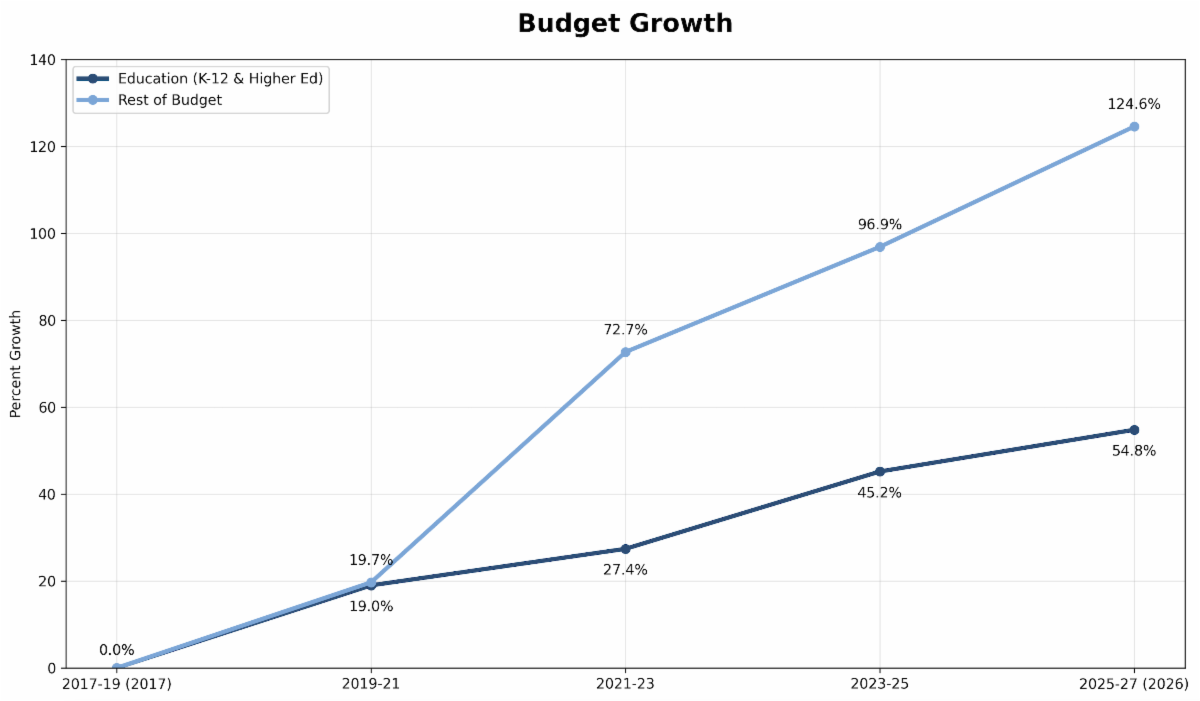

Not For Schools

Nearly every major tax increase proposed in Olympia is framed as an investment in education.

But recent budgets complicate that narrative.

Last year, lawmakers passed the largest tax increase in state history. Yet the share of the state budget devoted to education actually declined and now sits at one of the lowest levels in decades.

That does not necessarily mean education spending is falling in absolute terms. It means other parts of the budget are growing faster. That is where the income tax dollars are going.

If new taxes are consistently justified as investments in education, but education’s share of the budget keeps shrinking, voters are justified in questioning the veracity of what legislative leaders tell them year after year.

Federal Cuts Make Up Less Than 3% of the Tax

One of the most frequently cited arguments for the tax is that Washington must replace funding lost because of federal reductions associated with the so-called “Big Beautiful Bill.”

Washington’s share of these cuts included $173 million in administrative funding for the Supplemental Nutrition Assistance Program (SNAP) program, $171 million in cuts to SNAP benefits associated with new work requirements, and $14 million in cuts to family-planning funding.

That totals roughly $358 million over four years.

Now compare that with the projected revenue from the new income tax. State estimates indicate the tax will generate between $10 billion and $12 billion over the same period.

In other words, roughly 97 percent of the revenue raised by the tax has nothing to do with replacing federal cuts. If lawmakers simply wanted to backfill those reductions, they could have done so with a policy roughly thirty times smaller.

A Startup Ecosystem in Jeopardy

At the same time Washington is layering new taxes onto its system, Seattle’s competitive position in the innovation economy is changing.

The state has already seen how aggressive tax policy can influence behavior. When lawmakers dramatically increased estate-tax rates in recent years, many wealthy families began relocating to other states to avoid the tax. The migration became significant enough that legislators eventually planned to roll back portions of those increases.

However, even after those proposed changes Washington still maintains one of the highest estate-tax burdens in the nation.

Founders and high-growth companies now face overlapping taxes that collectively create one of the highest tax burdens in the country.

Since 2021, Seattle entrepreneurs have faced an avalanche of new taxes, including: “Jump Start” payroll tax (2021), capital gains tax (2022), social housing payroll tax (2024), capital gains surtax (2025), estate tax increase (2025), Seattle B&O tax increase (2025), state B&O tax increase (2025), and sales tax on services (2025). These are in addition to other local levies and regulatory burdens that have made Seattle the most expensive city in the nation on a host of metrics.

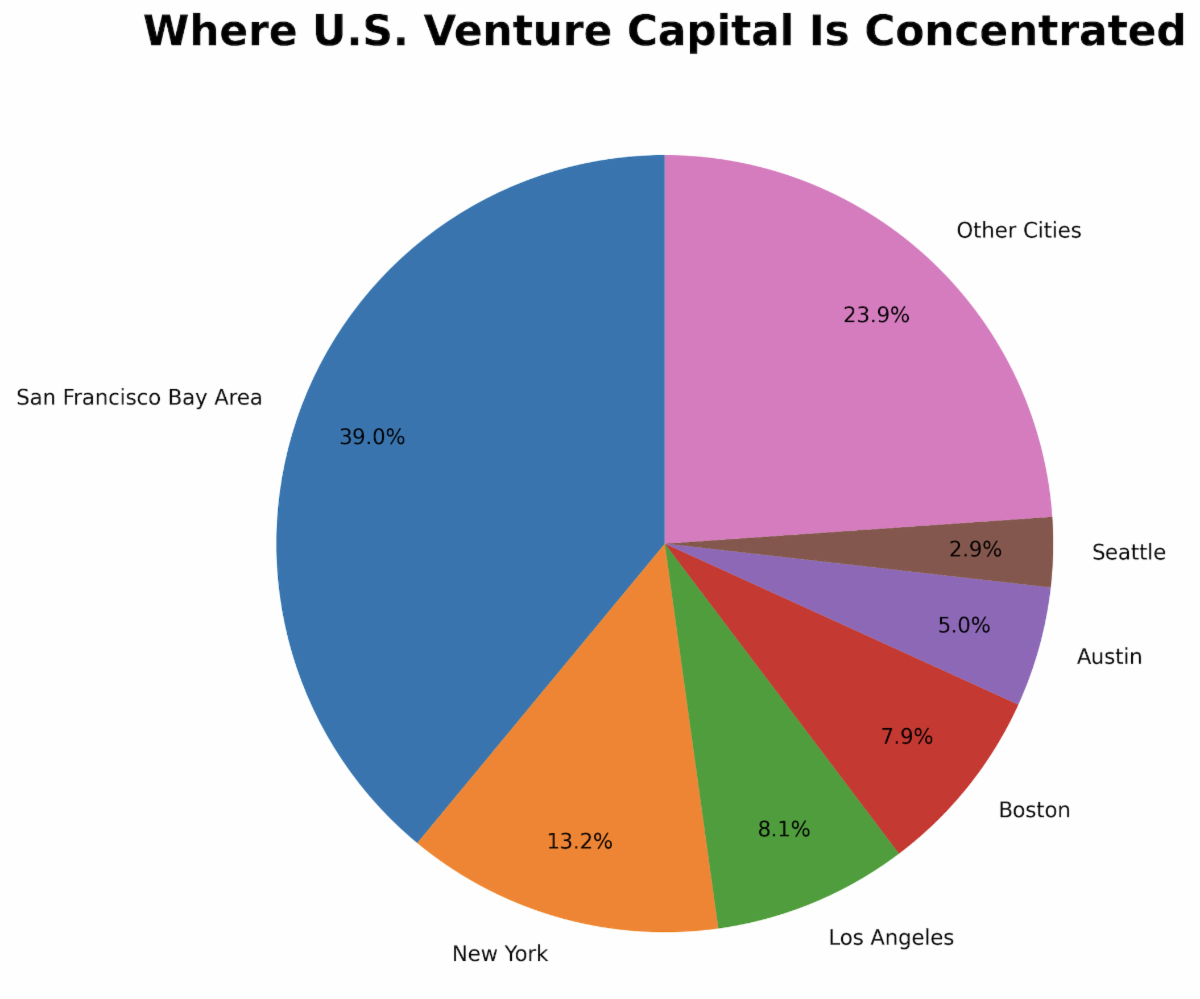

While we are now challenging the highest-taxed employment hubs in the nation, we fall well behind them in the concentration and availability of venture capital. The San Francisco Bay Area attracts roughly 45 percent of U.S. venture investment, New York about 20 percent, and Boston around 10 percent. The Seattle region typically attracts only about 3–4 percent.

For years the Washington Department of Commerce promoted the state to employers using a simple message. The pitch was straightforward:

- No personal income tax

- No capital gains tax

- Low electricity costs

- Affordable operating costs

- Generous tax exemptions and incentives

Over the past five years, policymakers have dismantled much of that strategy.

For years business leaders have warned that policies like these could erode Washington’s competitiveness. At this point the conversation is no longer about what might happen if the state fails to change course. We are already watching it unfold.

For smaller companies and individuals, the relocations have been largely quiet. They rarely make headlines but eventually show up when expected tax revenues fail to materialize.

For larger employers, the shift often begins with transferring small teams elsewhere. Amazon’s decision to build its second headquarters in Arlington, Virginia, and Starbucks relocating part of its product-development operations to Tennessee last week come to mind. The pattern is also visible in hiring data. Several of Washington’s largest technology companies have hired far more employees outside the state than within it in recent years. The state has already dropped to 35th in the nation for job growth with the state economist projecting flat private sector jobs by the end of the biennium.

“There won’t be press releases for the businesses that don’t open here or the jobs that aren’t created here.”

These decisions rarely happen all at once. They unfold gradually—one hiring decision, one relocation, one office at a time. There won’t be any press releases for the businesses that don’t open here or the jobs that aren’t created here. Over time the economic balloon that powered the region’s prosperity will slowly deflate. As it deflates, public-sector revenues shrink as well.

Governments will respond by raising tax rates to compensate for declining collections. That response will accelerate the very migration that caused the problem in the first place.

The new income tax will generate significant revenue. But the state’s own projections suggest it does not solve the structural pressures in the budget. Spending growth is on an unsustainable trajectory that will force the state into annual tax increases that the economy cannot sustain.

Our state’s political leaders have long believed that our economic dominance was either something we were entitled to or something that we created through deliberate policies. Neither is correct. We are thriving on the ecosystems created by entrepreneurs decades ago.

There are countless gold-rush logging towns whose story has turned out much different and less celebrated than ours. But other states and regions have awakened to the fact that luck isn’t enough and growing an economy that can fund effective government services and create a high quality of life takes intentionality and strategy.

Washington’s economic success was not inevitable. It was built over decades by entrepreneurs, innovators, and investors who chose to build here. Those choices are not guaranteed to continue.

If the state continues layering new taxes onto a rapidly expanding government, we may soon discover that the economic engine powering our prosperity is far easier to damage than it is to rebuild.

Today’s vote suggests our leaders are willing to take that risk.

Categories

Bellevue Chamber President & CEO Joe Fain: “In practical terms, this means taxpayers and employers from every corner of Washington would be directly subsidizing the City of Seattle’s budget.”

Read the editorial: https://lnkd.in/g-MttGZa

As we evaluate the legislation, we’re focused on affordability impacts for families and employers, whether outcomes are tangible in communities, and how the policy affects long-term budget sustainability and Washington’s competitiveness.

Chamber President & CEO Joe Fain also flagged several structural issues that need closer review, including treatment of pass-through entities, charitable deductions, a potential marriage penalty, and interactions with other state tax policies.

Read more: https://lnkd.in/g8Uv_wD4